Prairienomics Signal Pack - Week of Mar 28 : Two months late. 27 days of Hormuz. Urea past US$690. Bond yields surging. Seven things the farm CFO needs right now, plus the indicator dashboard and deadline calendar.

This is the first Signal Pack in two months. It should not have taken this long. The plan was to launch in January, and I did not execute. That is on me.

In the meantime, the world handed Prairie agriculture its most consequential 26-day stretch since the 2022 Russia-Ukraine shock. Rather than pretend I was not gone, this week's pack covers the full window, February 28 through March 26, so everyone is starting from the same page. Going forward, this lands every Friday.

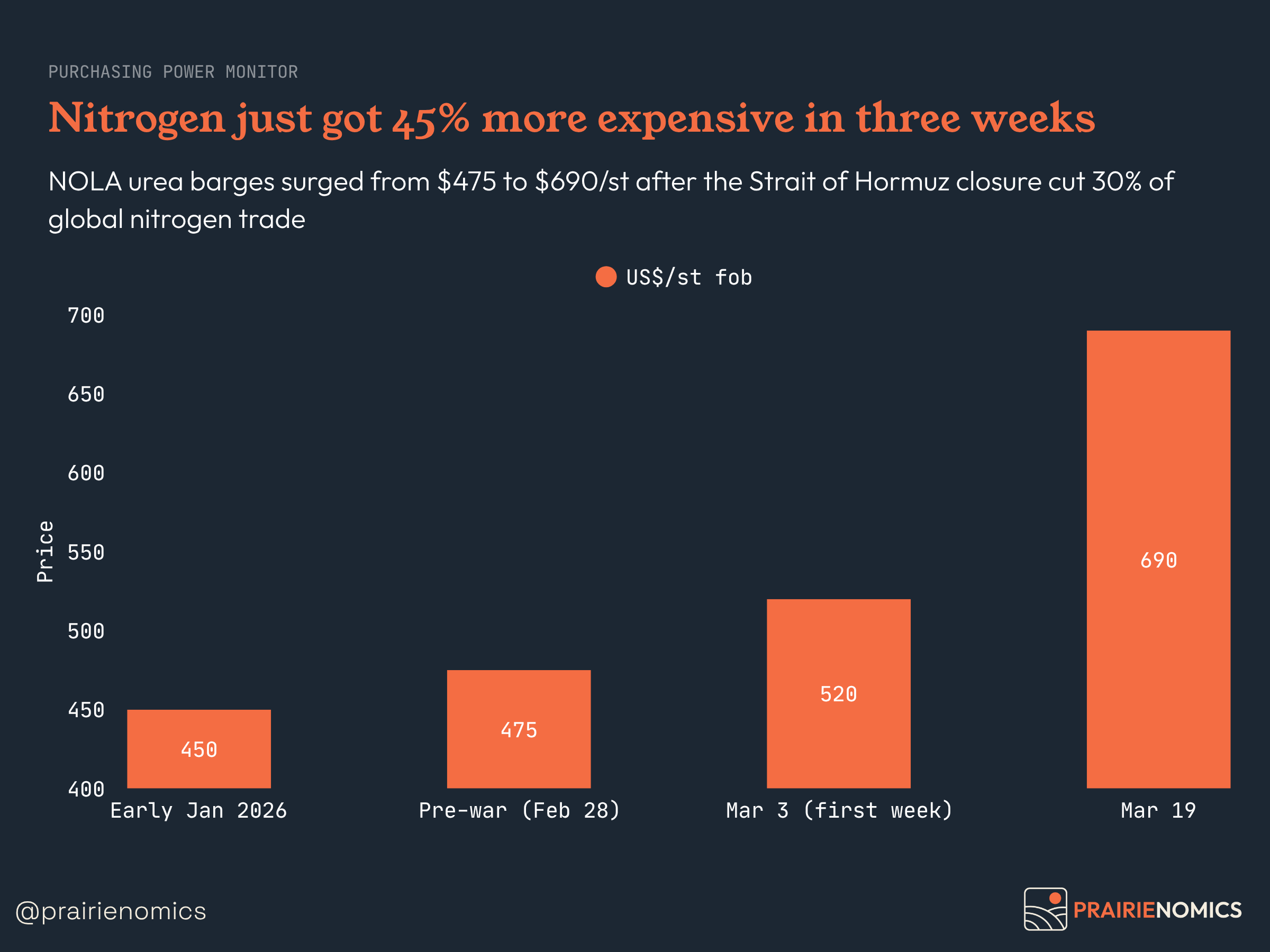

🟠 Day 27. No resolution. Fertilizer prices still climbing. Before the Strait of Hormuz closed on February 28, a barge of urea at New Orleans cost about US$475/st. Three weeks later it was past US$690. DTN's national retail anhydrous ammonia average hit US$931/ton in the third week of March, with the Illinois AMS report showing prices as high as US$998. The reason is not complicated. Roughly 30% of the world's traded urea moves through the Strait, and right now it is not moving. QatarEnergy shut down urea production entirely. China will not export until August. There is no backup supply sitting in a warehouse somewhere. A vessel that loaded in the Gulf today would not reach North American shores until mid-April, which is after most of the spring application window has closed. If you locked in nitrogen before February 28, none of this touches you. If you did not, add C$15-35/ac to your canola input budget. On 5,000 acres that is C$75,000-C$175,000 that was not in the plan a month ago.

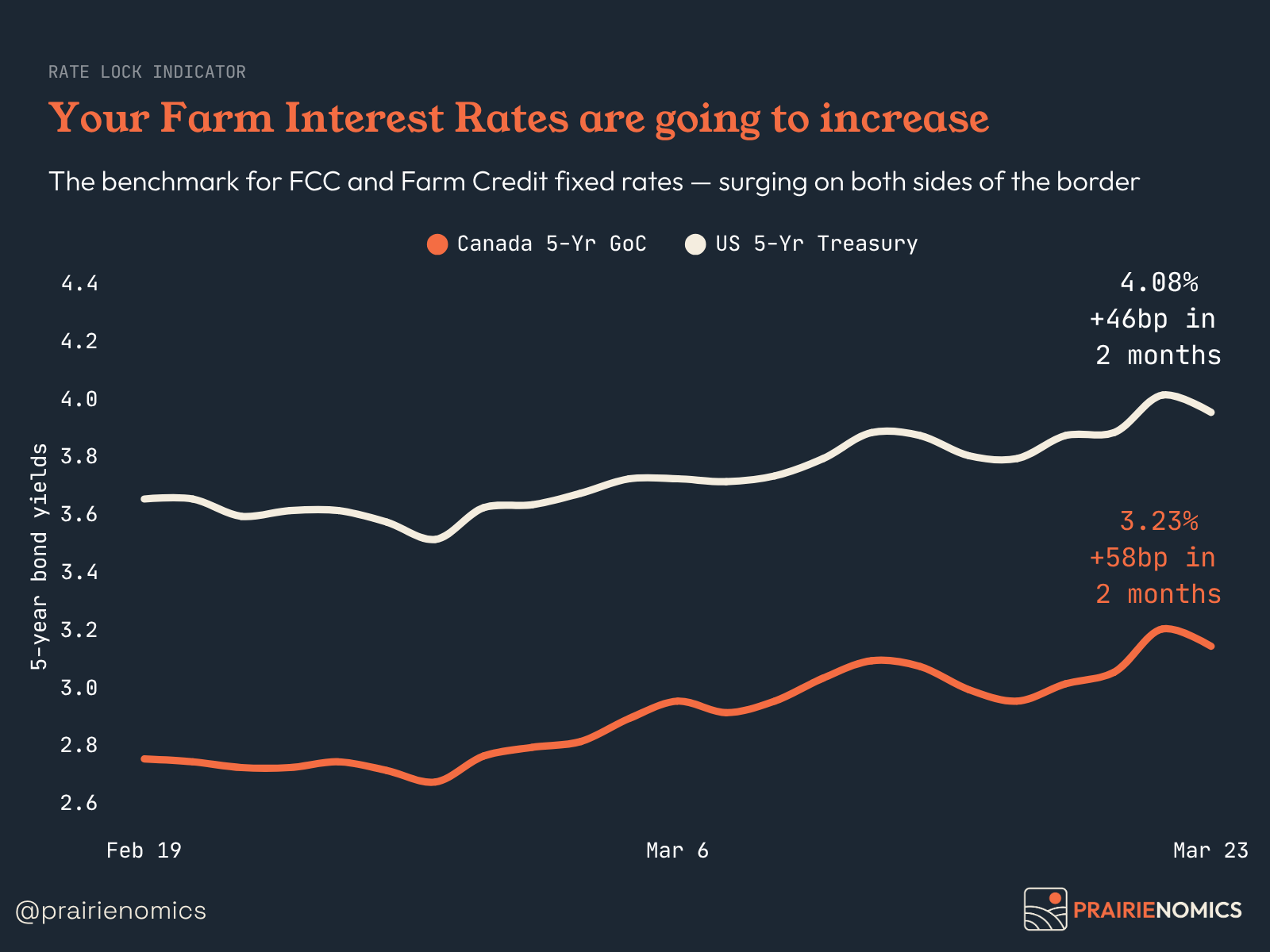

🟠 Both central banks held rates. Bond markets did not. The BoC stayed at 2.25%. The Fed stayed at 3.50-3.75%. The headlines said "no change" and moved on. But the number that actually sets your FCC fixed rate, the GoC 5-year bond yield, quietly climbed 54 basis points in a single month to 3.20%. That is the largest monthly move since early 2023, and it translates almost directly into higher fixed farm lending rates. A C$2M land loan locked in today costs roughly C$10,000/yr more than the same deal four weeks ago. A C$500K operating line converted to term, about C$2,500/yr. Macklem was unusually blunt about why the BoC is stuck: cutting rates would let energy-driven inflation run, but hiking would crush an economy that already lost 84,000 jobs in February. He warned that March CPI will show inflation rising. For the first time since 2023, markets are pricing a possible rate hike by October. The direction of the next move is genuinely uncertain, and that uncertainty is itself a cost for anyone carrying variable-rate debt.

🟠 Canola futures rallied. Cash prices barely moved. The gap tells the real story. ICE canola May hit C$703/t on March 26, up C$38 from where it sat before the Hormuz crisis. The Carney-Xi tariff deal is doing real work here, with seed tariffs cut from roughly 85% to ~15%, and domestic crush margins are strong with capacity running at 90% utilization. By the futures board, canola looks great. But walk into a Moose Jaw elevator and the picture changes. Terminal cash canola rose only C$13/t over the same window. That C$25/t gap between what the board says your canola is worth and what you actually get paid exists because CPKC delivered just 52% of shipper-ordered hopper cars in early March. Three weeks running, worst performance of the crop year. Record volumes are moving through the system but the system is full, and when it is full the producer absorbs the cost through wider basis.

🟠 The worst US winter wheat drought in 20 years is bullish for Canadian exports. Over half of US winter wheat acres are now in drought. The March 24 monitor shows 57% in D1 or worse, conditions have not been this poor this early in the season since at least 2002, and a persistent heat dome has been running Plains temperatures 20-25°F above normal for weeks. The Morrill Fire in Nebraska burned over 800,000 acres. Hard red winter wheat is already trading its widest premium to soft red in nearly a year. None of this has shown up in official production estimates yet because the first USDA winter wheat forecast does not come until the May WASDE. But the direction is obvious. If US production comes in short, global importers look to Canada, Australia, and the EU. Prairie spring wheat and durum stand to benefit on the export side heading into summer.

🟠 The Supreme Court gutted the President's tariff authority. Now USMCA is everything. On February 20, SCOTUS ruled 6-3 that IEEPA does not authorize tariffs. That single decision struck down the legal basis for the Liberation Day tariffs and removed the most powerful unilateral trade tool the President had. Trump replaced them within hours with 15% Section 122 tariffs, but those expire after 150 days on July 24 unless Congress extends them. USMCA-compliant Canadian agricultural goods remain duty-free under both regimes, which covers most of what the Prairies export south. The question is what happens next. The USMCA review deadline is July 1. Forty US agricultural organizations have already formed a coalition to defend the agreement, citing US$149 billion in domestic economic activity from ag exports to Canada and Mexico, which tells you the threat is being taken seriously on both sides of the border. If USMCA is terminated or weakened, every bushel crossing into the US gets more expensive. That is the single largest structural trade risk on the Prairie calendar this year, and it is 97 days away.

🟠 AgriStability enrollment closes April 30. The program got less generous at the wrong time. Last year's temporary deal, 90% compensation and a C$6M cap, is gone. 2026 reverts to 80% and C$3M. New for 2026, pasture rental costs are now allowable expenses and feed inventory pricing was adjusted for livestock operations, but neither of those changes the calculus for grain. What changes the calculus is the input cost environment. Nitrogen is up 18-42% year over year. Diesel is within two cents of its all-time high. The AgriStability trigger fires when your margin drops more than 30% below your historical reference. With input costs running this far above where they were when your reference margins were built, that 30% decline is not a worst-case scenario. It is a plausible one. The enrollment fee is a few hundred dollars. Enroll.

🟠 USDA Prospective Plantings drops Monday. March 31 at noon ET, alongside quarterly Grain Stocks. This is the most market-moving report between now and the May WASDE. Private analysts expect the largest corn-to-soybean acreage shift in years, with corn acres potentially down 4-5% from 2025's 9-decade high and soybeans up roughly 6%. The logic is straightforward: soybeans cost less to plant than corn, and the Hormuz fertilizer spike made the gap wider. Spring wheat acres are expected down as well. The catch is that most survey responses were collected before the worst of the price shock hit, which means actual planting decisions on the ground may be leaning even further toward low-input crops than this report will capture. Monday's number will set the tone. The real picture will not be clear until the June Acreage report.

Sources: Profercy World Nitrogen Index, DTN Retail Fertilizer Index, USDA AMS Illinois Production Cost Report, Trading Economics, Investing.com, PDQ via CKRM, Ag Transport Coalition, US Drought Monitor, High Plains Journal, Bloomberg, SCOTUSblog, Holland & Knight, PIIE, CBC, AAFC, Government of Saskatchewan, AgMarket.Net, StoneX.